Applying for a loan can feel daunting, but understanding one simple concept can make a real difference: your Debt Service Ratio, or DSR. DSR measures how much of your income already goes toward debt repayments, and it is one of the first things banks look at when assessing whether to approve your loan.

Here is what DSR is, how it is calculated, and how to keep yours healthy.

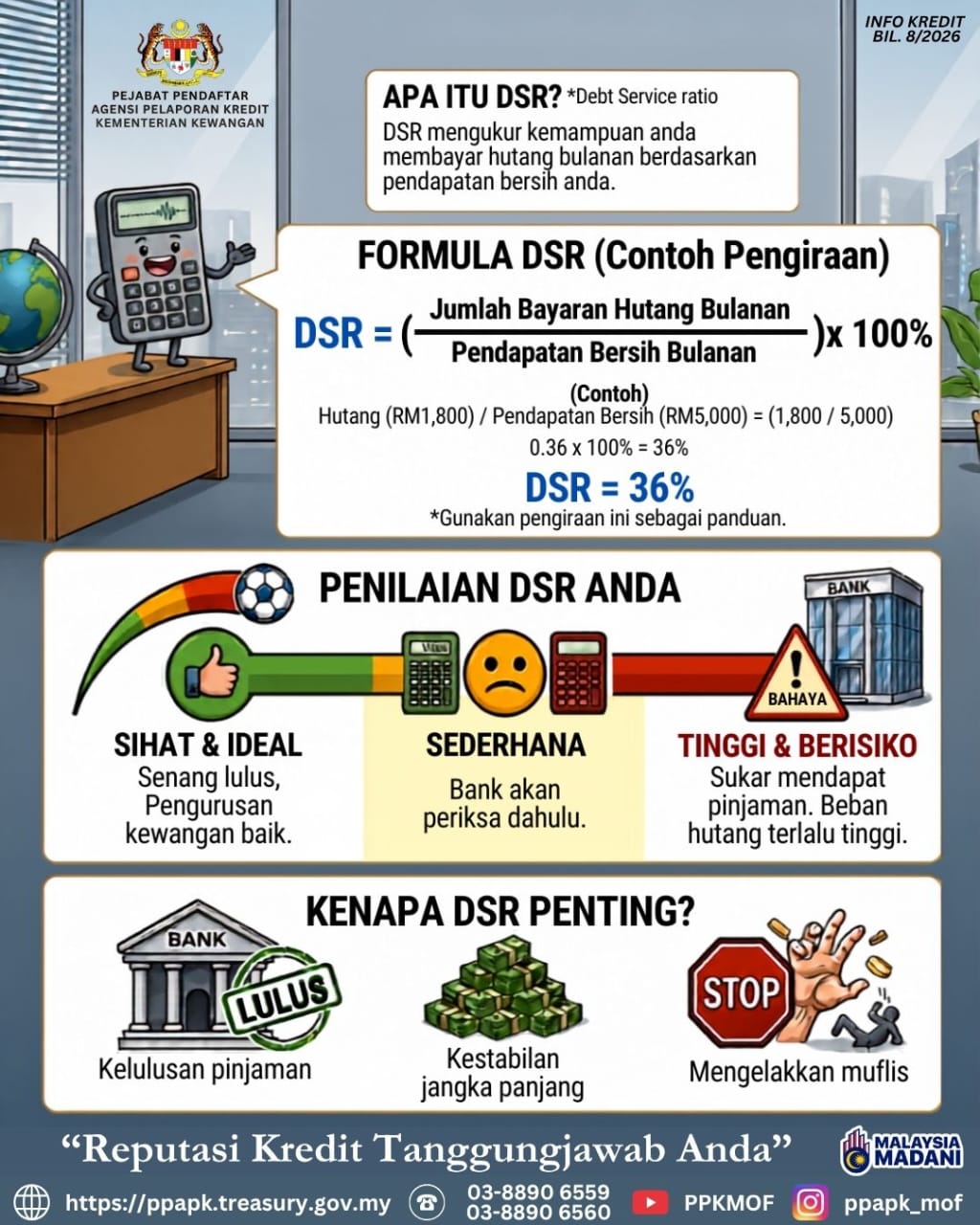

What Is DSR?

DSR (Debt Service Ratio) measures your ability to pay your monthly debts based on your net monthly income. It is expressed as a percentage.

The formula is straightforward:

DSR = (Total Monthly Debt Payments ÷ Monthly Net Income) × 100%

A Simple Example

Say your total monthly debt payments (credit card minimums, car loan, personal loan, and any other regular repayments) add up to RM1,800. Your monthly net income is RM5,000.

DSR = (RM1,800 ÷ RM5,000) × 100% = 36%

That means 36% of your net income is already committed to servicing debt each month. The lower your DSR, the more comfortable a bank feels about lending you more.

Visual credit: Registrar Office of Credit Reporting Agencies, Ministry of Finance (Info Kredit Bil. 8/2026).

Understanding Your DSR Level

Your DSR percentage tells you where you actually stand with banks. Here is how it generally breaks down in Malaysia, based on how lenders assess risk:

- Below 30%: you are in excellent financial shape. Banks see you as a strong, low-risk borrower with the fastest approval path and access to the best interest rates. Your borrowing power is high, and you can comfortably take on larger loan amounts.

- Between 30% and 40%: this is the sweet spot. You are managing your debt responsibly and still have comfortable room in your income. Banks approve you easily for most loans and are usually happy to lend generously.

- Between 41% and 60%: you are entering the cautious zone. This is around the upper DSR limit most banks accept for middle-income borrowers. Lenders become more careful and may reduce the loan amount they are willing to offer. If you are planning a major application, this is a good time to clear smaller debts first.

- Between 61% and 70%: you are considered financially stretched. At this level, approval is only likely if you have a high net income or the loan is secured by collateral, such as a house. Reducing debt or considering a joint application is often the more realistic path forward before applying for anything new.

- Above 70%: you are heavily over-leveraged. Banks view this as a serious risk because there is very little disposable income left for daily living and unexpected expenses. New loan applications at this level are almost always rejected, and the priority should be reducing existing commitments before considering any new borrowing.

Note:

Each bank sets its own internal DSR limits, and the acceptable range can vary depending on income level and loan type. But the underlying principle is the same everywhere: the lower your DSR, the more comfortable a bank feels lending to you.

Why DSR Matters

- Loan approval: a healthy DSR significantly improves your chances of getting approved.

- Long-term financial stability: keeping DSR manageable means your monthly commitments do not stretch beyond what your income can comfortably support.

- Avoiding bankruptcy: high DSR is a warning sign that debt is accumulating faster than income can service it.

How to Improve Your DSR

- Clear smaller debts first. Even eliminating one credit card or personal loan can meaningfully shift your DSR.

- Reduce credit card balances. Minimum payments on cards count as fixed commitments in DSR calculations, even at zero balance.

- Avoid stacking new applications in the months before a major loan.

- Review your CCRIS Record to see every active credit facility contributing to your DSR. This is where the bank sees your commitments too.

Know Where You Stand Before You Apply

Your CCRIS Record inside your MyCTOS Score Report shows every active credit facility under your name, which is the starting point for calculating your DSR. Reviewing it alongside your CTOS Score gives you the fullest picture of what banks will see before you submit any loan application.

FAQ

What is a good DSR in Malaysia?

Generally, a DSR below 40% is considered healthy, with anything below 30% viewed as excellent. Between 41% and 60% is where banks start becoming more cautious, and anything above 60% is typically treated as high-risk. Each bank sets its own thresholds, but the lower your DSR, the more comfortable a bank feels lending to you.

Does DSR use gross or net income?

According to the Registrar Office of Credit Reporting Agencies, DSR is calculated using your net monthly income, meaning income after statutory deductions such as EPF and tax.

Where can I see the debts that count toward my DSR?

Your CCRIS Record, included in your MyCTOS Score Report, lists every active credit facility under your name along with the monthly commitment attached to each. It is the most reliable starting point for calculating your DSR.

Does checking my own Credit Report affect my DSR?

No. Checking your own CTOS Report is a personal inquiry and has no impact on your CTOS Score or your loan applications. Only credit applications submitted to lenders create inquiries visible to other banks.

{kind=link}

{kind=link}

{kind=link}